Perfect Competition

Perfect competion

Is a market structure in which uniform price is charged for every unit of a good.

Assumptions of perfect competition

a. Homogeneous product

b. Large numbers of buyers and sellers

c. Free entry and exit

d. Free mobility of factors of production

e. Perfect knowledge

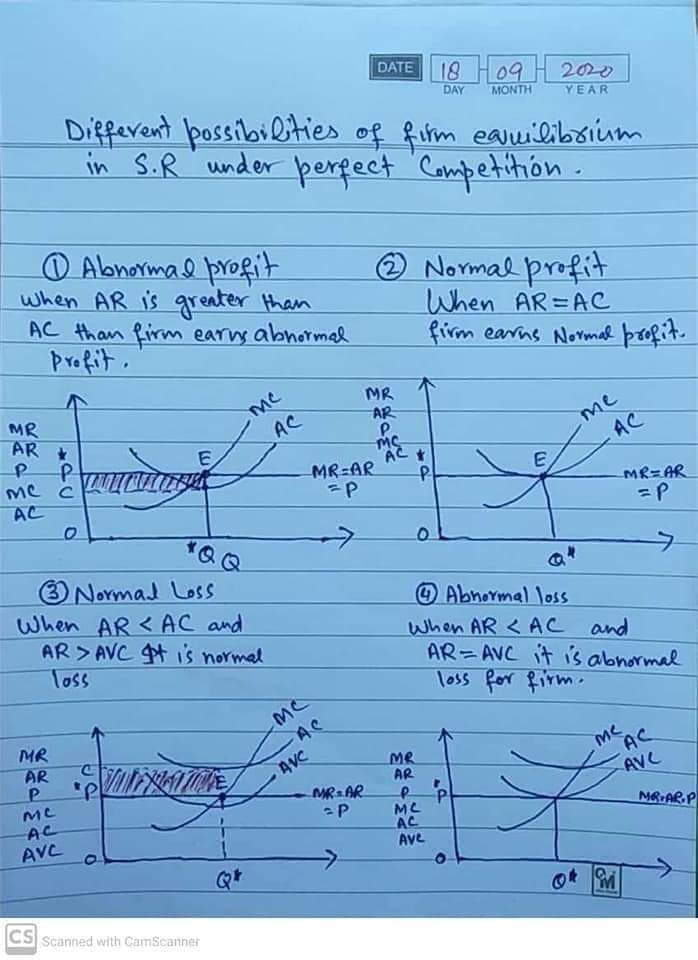

Firm equilibrium in short run under perfect competition

There are two ways for firm equilibrium

a. Total revenue and total cost approach

b. Marginal revenue and marginal cost approach

Explanation

a.TR and TC Approach

According to this approach a firm will be in equilibrium when the difference between total revenue and total cost is maximum and firm will select the that level of output where difference is maximum.

b. MR and MC Approach

According to this approach a firm will be in equilibrium where the MR is equal to MC.

There are two conditions for firm equilibrium

i) Necessary condition

MR=MC

ii) Sufficient condition

At equilibrium point slope of MC must be greater than slope of MR, in other words MC must cut MR curve risingly.

Comments

Post a Comment

Please write a sensible comment. Do not humiliate others.